HOW TO INVEST MONEY IN UAE: BEST INVESTMENT OPTIONS IN THE COUNTRY | CAonWeb.com Investing your hard earned money has always been a top priority for every individual. Each and every individual looks forward to most optimum investing opportunity to park their funds. Depending on the risk bearing capacity and the amount of funds in […]

GST REGISTRATION PROCESS IN INDIA

Goods & services tax viz. is popularly known as GST is a form of indirect taxation method prevailing in the India. Government of India rolled out the new format of indirect taxation on 1st July, 2017 by pushing aside the earlier regime of Value added tax (VAT). The idea of having GST is to transform […]

WHY CHOOSE PRIVATE LIMITED COMPANY REGISTER IN INDIA

Private limited company registration in India is one of the most opted out business structures by Startups and new ventures. One of the most centralized and organized form of company registration in India which borrows its procedure from companies act, 2013 viz. is directly governed by Ministry of corporate affairs (MCA). What is Private Limited […]

COMPANY REGISTRATION IN DUBAI

Simple & easy way of online company registration in Dubai Company registration in Dubai has always been a bone of contention for almost every potential Startup who wants to get online company registration in Dubai; but not anymore!! In the 21st century of globalization, every business that is planning to get their hands on the […]

TRUST REGISTRATION IN INDIA

Trust/NGO stands for Non-government organization which is formed to serve the society in general and towards a social cause in particular. It is referred as non-governmental because they work for the social welfare of the society with no prior motive of earning a profit in their activities. Mostly, NGO are privately funded through donations, charity […]

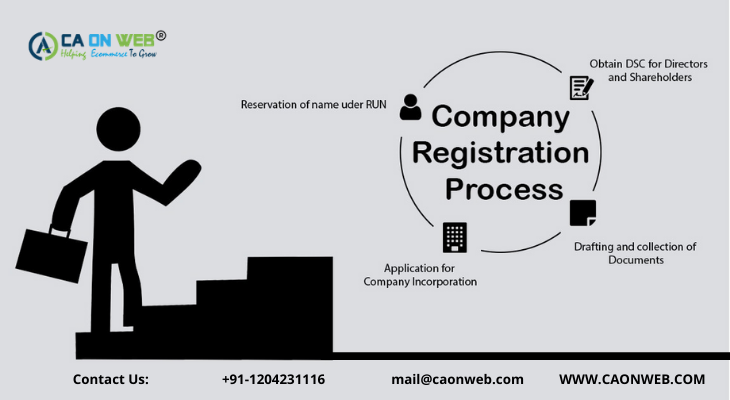

COMPANY FORMATION IN INDIA

One of the fastest growing economies is India which makes it profit lucrative place for a private limited company registration in India. Ease of doing business is one of the pre-requisites which almost every rational business looks forward during their initial stage of company registration in India. Therefore many Startups are choosing to register under […]

SIMPLE STEPS OF COMPANY REGISTRATION IN DUBAI

Guiding you through the most optimum business structure of the company registration in Dubai. ‘With expanding economies, comes the desire to expand your businesses. Economies are expanding so does the desire of Startups/businesses to expand their business and the most lucrative place they find most attractive to expand their business is Dubai. Company registrations in Dubai […]

PRIVATE LIMITED COMPANY REGISTRATION IN INDIA

How a private limited company registration is suitable for Startups in India? Startups require a different and unique business environment to function and India exactly possesses the same. Capital flexibility, no. of directors, fund raising for business and easy procedures to hold business meetings and carrying AGM’s are some of the benefits being forwarded to […]

RULES & REGULATIONS OF ARBITRATION PROCEEDINGS IN INDIA

WHAT IS ARBITRATION? In simple terms, Arbitration is an informal form of the judiciary that helps in resolving the dispute between two or more than two parties. Arbitration is a legal procedure in which both parties refer their dispute to one or more arbitrators which implies a binding decision on both parties. Arbitration proceedings in India are […]

SIMPLE STEPS OF COMPANY REGISTRATION IN INDIA

A complete beginner’s level guide for Startup India registration We all have a creative & unique business idea with us; and we all have a big shot dream of staring our own venture. But what is pulling all of us back is lack of adequate knowledge and direction needed to go for Startup India registration. […]